Taxes5 min read

Dividend Taxes Explained: What Every Investor Must Know

Understand how dividends are taxed, the difference between qualified and ordinary dividends, and strategies to minimize your tax burden.

Jan 13, 2025 Read More

Understand how dividend reinvestment creates exponential wealth growth through compounding, and learn strategies to maximize this powerful effect.

Albert Einstein reportedly called compound interest "the eighth wonder of the world." When applied to dividends, compounding becomes an incredibly powerful wealth-building tool. Here's how it works and how to harness it.

Dividend compounding occurs when you reinvest your dividends to buy more shares, which then generate their own dividends, which buy more shares, and so on. It's a snowball effect that accelerates over time.

Simple example:

Future Value = P × (1 + r)^n

Where:

| Scenario | Final Value | Total Dividends |

|---|---|---|

| 3% yield, no reinvestment | $10,000 + $9,000 dividends | $9,000 |

| 3% yield, reinvested | $24,273 | $14,273 |

| 4% yield, reinvested | $32,434 | $22,434 |

| 4% yield + 5% growth, reinvested | $66,439 | $56,439 |

The difference between reinvesting and not reinvesting is dramatic—and adding dividend growth makes it extraordinary.

Your initial yield determines the base of your compounding. Higher yields mean more dividends to reinvest from day one.

Impact of starting yield on $10,000 over 20 years (reinvested):

Companies that increase dividends annually supercharge compounding. Your yield on cost grows over time.

$10,000 at 3% yield with different growth rates (20 years):

Time is the most powerful factor. The longer you compound, the more dramatic the results.

$10,000 at 4% yield, 6% dividend growth:

The last 10 years produced more wealth than the first 30 combined.

Yield on Cost (YOC) measures your dividend income against your original investment. As dividends grow, your YOC increases even if the stock's current yield stays flat.

Example:

You're earning 12% annually on your original investment while new buyers only get 3%.

A quick way to estimate how long it takes to double your money:

Years to Double = 72 / Annual Return

Examples:

If you invested $10,000 in Coca-Cola (KO) in 1994:

Your yield on cost would be over 23%—you'd be earning 23% annually on your original $10,000 investment.

The earlier you start, the more time compounding has to work.

Starting at different ages with $500/month, 7% return:

Starting 10 years earlier more than doubled the final amount.

Enable automatic dividend reinvestment (DRIP) and resist the temptation to spend dividends.

A 2% yielder growing dividends at 10% annually will outperform a 5% yielder with no growth—given enough time.

Regular contributions amplify compounding. Even small amounts add up dramatically over decades.

Selling resets your compounding clock. Long-term holding lets the snowball keep growing.

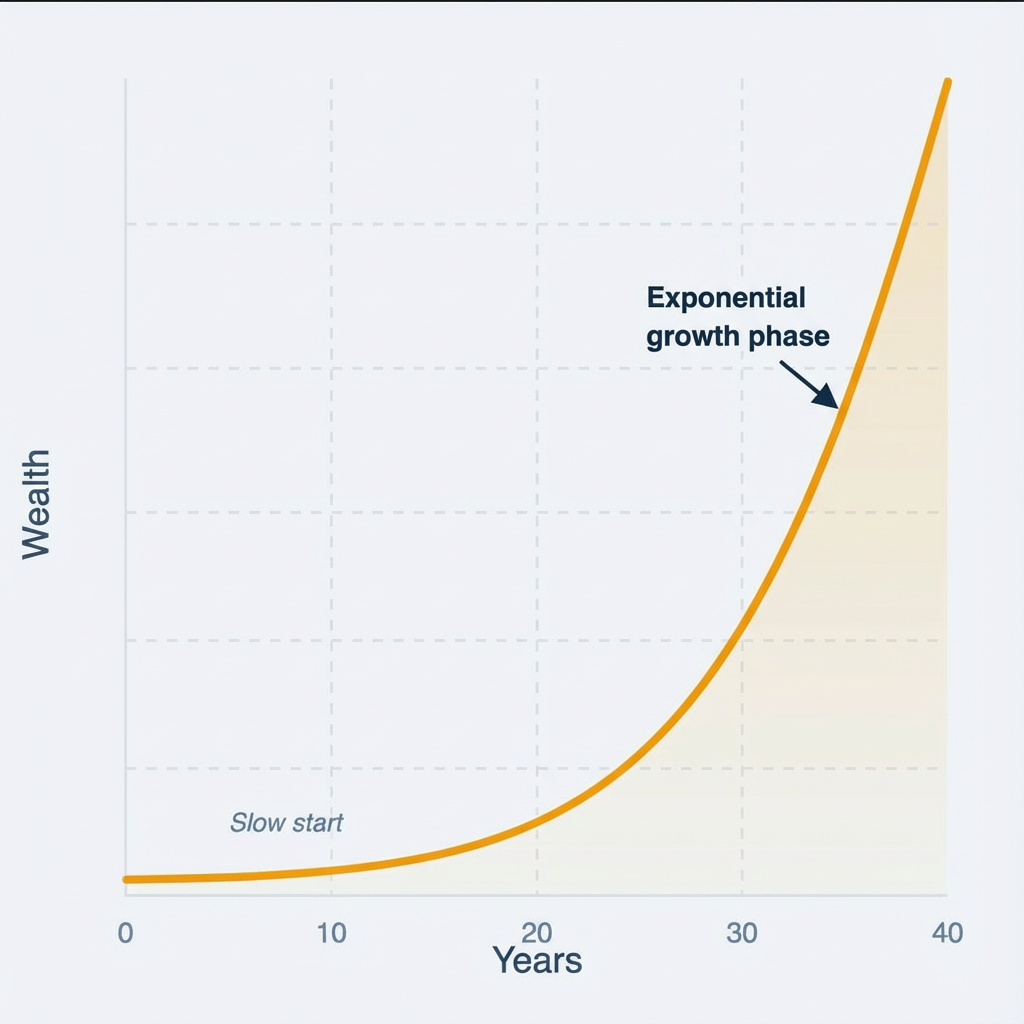

Compounding growth isn't linear—it's exponential. The curve looks like a hockey stick:

The first 10-15 years feel slow. The last 10-15 years feel explosive. Most people quit before reaching the steep part of the curve.

Every year you delay costs you exponentially in the long run. Start now, even with small amounts.

Using dividends for expenses breaks the compounding chain. If you need income, use a different strategy.

A 10% yield that gets cut does nothing for compounding. Sustainable growth beats unsustainable yield.

Every sale is a taxable event that removes money from compounding. Buy and hold works better.

Compounding rewards patience. The magic happens in decades, not months.

Compounding works best in accounts where taxes don't take a bite:

Use calculators to see compounding in action:

Seeing the numbers makes the math feel real and motivates long-term thinking.

Put compounding to work:

Use our dividend calculator to see exactly how compounding will grow your specific portfolio over time.

Understand how dividends are taxed, the difference between qualified and ordinary dividends, and strategies to minimize your tax burden.

Learn to use AI chatbots like ChatGPT and Claude to screen dividend stocks with copy-paste prompts, verification checklists, and hallucination safeguards.

Use AI to generate, backtest, and compare dividend strategies with repeatable prompts. Includes a quarterly review workflow and strategy templates.

Compare the best platforms for dividend investing or calculate your potential passive income.